內容目錄

業績分析

Revenues: For the quarter, net revenues grew 10% to $9.5 billion, resulting in net revenues ahead of 2019, and organic revenues (non-GAAP) grew 9%. Revenue performance included 10% growth in price/mix and a decline of 1% in concentrate sales. The quarter included six fewer days, which resulted in an approximate 6-point headwind to revenue growth. The quarter was also impacted by the timing of concentrate shipments. For the full year, net revenues grew 17% to $38.7 billion, and organic revenues (non-GAAP) grew 16%. This performance was driven by 9% growth in concentrate sales and 6% growth in price/mix.

收入按季上升10%,按年上升17%。

Margin: For the quarter, operating margin, which included items impacting comparability, was 17.7% versus 27.2% in the prior year, while comparable operating margin (non-GAAP) was 22.1% versus 27.3% in the prior year. For the full year, operating margin, which included items impacting comparability, was 26.7% versus 27.3% in the prior 1 year, while comparable operating margin (non-GAAP) was 28.7% versus 29.6% in the prior year. For both the quarter and the full year, operating margin compression was primarily driven by a significant increase in marketing investments versus the prior year. Additionally, fourth quarter operating margin was impacted by topline pressure from six fewer days in the quarter along with the timing of concentrate shipments.

營業利潤率按季上升27.2%,按年上升27.3%。

稅後盈餘還是每股淨利按年都上升26%。

按分區來說,稅前收入貢獻最多的是一個叫Bottle Investments的灌漿業務部份,按年上升78%約9億,為什麼會有這麼大的升幅,這個部分感覺不太能夠持續,可能要繼續留意。

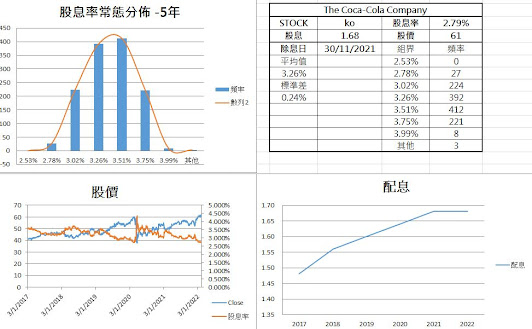

股息率 (殖利率)常態分佈-5年圖

接下來我們算一下股息的分發,現價股息率約2.79%,歷年payout ratio一貫保持在80%的範圍,2021年曾經有達到95%,現在業績有增長,即使全年增長27%,預計股息增長多於10%的機會也不大,我們以1.68×110%=1.848來估算,股價也就是56.68。現價61元是預計股息有18.3%的增長,即全年股息為1.987,每季為0.496,個人會認為這個機會不大,畢竟未來不會是一個容易經營的經濟週期,管理者選擇多留一些資金儲備會更理想。從股價來看,因為consumer defensive板塊和業績增長的關係,股價這一段大升幅已經把價值都price-in進去,現價入場不是一個很好的選擇。

如何利用定量分析算出可口可樂的合理買入點?

針對可口可樂(KO)這類成熟的配息股,利用定量分析來避開情緒波動是至關重要的。我們可以透過「股息分發能力」與「YieldSpot 息率分位儀」的即時數據,來精確定位目前的投資價值。

1. 股息增長預估與定價邏輯

我們首先觀察 KO 的財務基本面。目前 Payout Ratio(派息率)為 67%,處於非常健康的範圍(低於歷史常見的 80%),這顯示公司有充足的空間維持連續 23 年(自 2003 年起)的增配紀錄。

然而,即便公司業績有所增長,基於定量保守原則,預計股息增長要超過 10% 的機會並不大。我們進行以下測算:

- 保守預估(增長 10%): 以目前的股息計算,對應合理股價約為 $64.12。

- 市場現狀: 當前股價已來到 $76.41,這意味著市場溢價已遠超基於股息增長的基礎估值。

2. YieldSpot 數據:歷史分位數的警示

根據 YieldSpot (息率分位儀) 的最新定量模型顯示,可口可樂目前的投資評價為 「暫緩布局」:

- 當前股息率: 2.70%。

- 歷史分位: 僅處於 2.6% 的極低水位(門檻為 55%)。這代表在歷史長河中,現在的 KO 比 97% 的時間都要「貴」。

- 進場門檻: 定量模型建議的理想進場殖利率為 3.27%(即需回到 > 55% 分位數)。

3. 定量分析結論:耐心是最好的策略

雖然 KO 的模型評分高達 4.5/5.0(代表公司質素極佳、信心度高),但目前的股息率處於歷史低位,並非最佳進場時機。

- 合理買入點判斷: 根據殖利率均值迴歸理論,當股價遠高於根據安全邊際推算的區間,且殖利率分位低於 25% 時,風險回報比並不理想。

- 操作建議: 現價 $76.41 已充分反應(Price-in)了防禦性板塊的漲幅。投資者應耐心等待股息率回升至 3.27% 以上的水平,屆時再行布局,才能確保長線復利的穩定性。

「Charlie chacha,Excel VBA 愛好者、馬拉松跑者、

長線投資人。

🔧 目前在做:

📡 Yieldspot | 息率分位儀 <– 歡迎試用

— 幫存股族了解股息率歷史分位位置的分析工具」